- Some Florida lawmakers want to extend the time state workers would be allowed to “double-dip” by collecting retirement benefits even while still employed in their state jobs.

- Florida elected officials – including state lawmakers – are also eligible to participate in the double-dipping program, known as the Deferred Retirement Option Program (DROP).

- The bill will make it harder for the private sector to attract and retain talent because the state benefits are so lucrative.

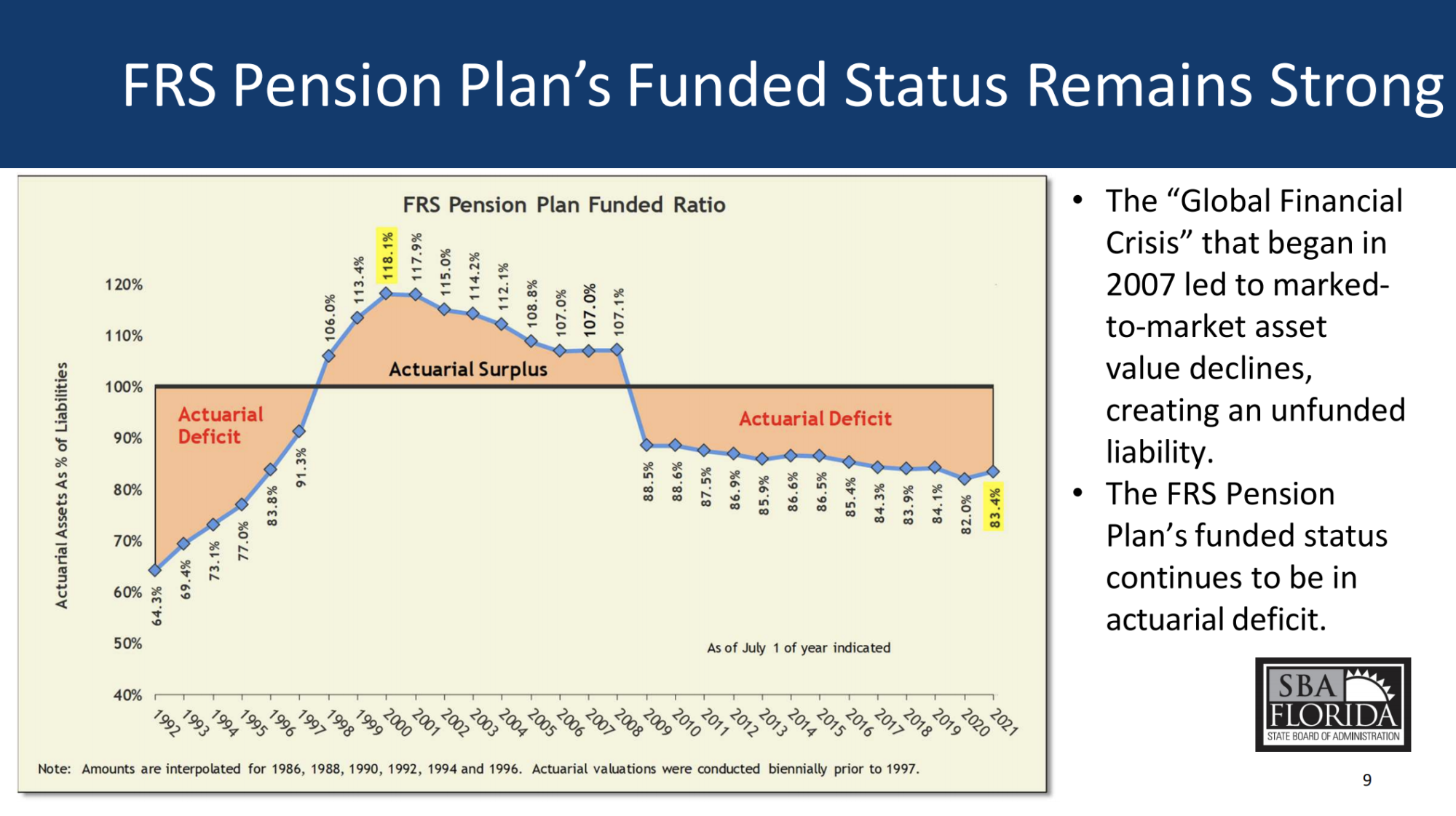

- The Florida Retirement System (FRS) already faces a $36 billion debt and is only 82% funded.

- The bill will cost taxpayers $3.1 billion in the upcoming fiscal year and do little to address FRS’s unfunded liabilities.

On Tuesday of last week, the Florida House Appropriations Committee voted to advance a bill aimed at significantly expanding state retirement benefits with the goal of attracting and retaining state workers – particularly police officers, firefighters and other first responders, but also teachers and some 90,000 state bureaucrats – because the vacancy rate for those jobs is currently over 16 percent.

The current plan to address the worker shortage includes an expansion of the controversial Deferred Retirement Option Program, known as DROP, which allows state bureaucrats who’ve reached retirement age to “double dip” by collecting retirement benefits even though they haven’t actually retired. The retirement payments go into a special bank account, where they can also earn interest, too. Under current rules, the state allows employees to remain in the DROP program for five years. But HB 239 would allow DROP participants to collect retirement benefits while keeping their job for up to 8 years, and it doubles the interest they currently earn on those retirement funds while they’re employed.

In defending the bill, Republicans are sticking to talking points centered around first responders, but the excuse doesn’t quite make sense when it comes to DROP benefits.

“These restrictive windows prompted many public employees including our law enforcement officers and first responders to retire before they were ready,” says State Rep. Demi Busatta Cabrera. “These changes will help our state and local governments and departments to retain experienced staff for a much longer period of time.”

Indeed. And yet, the bill goes out of its way to ensure “special risk class” members in the retirement system, which includes police and firefighters, can “retire” five years before regular members like elected officials and teachers. During testimony on Tuesday, one firefighting association thanked lawmakers for allowing them to retire early so they aren’t exposed to five additional years of dangerous chemicals, PTSD or other trauma. So for police and firefighters, the DROP program, which would entice them to stay and work even longer, seems to run counter to the very logic police and firefighters used to convince lawmakers to reduce the years they’re required to work before they can retire.

If there’s one class of state employee that might be a worthy recipient of the DROP program, its teachers. In that case, DROP might help address the ongoing workforce shortage. For virtually every other class, DROP is just another way to game the system and rake ever more cash out of FRS.

So allowing access to the controversial DROP program is bad enough, but HB 239 expands the benefits of DROP across the board, allowing any and all state employees who reach retirement age, no matter how critical (or not), to double-dip from the system for up to eight years. And that’s not the only change: the bill will also increase the interest rate earned on their double-dipped dollars from 1.4 percent to 4 percent.

The original intent of the DROP program was to allow the state to retain rare skill-sets and experience in mission-critical jobs that are essential to the state. That argument makes sense in certain situations, and perhaps for highly-specialized jobs when there simply isn’t a new crop of fresh, young workers to come in and fill those positions. But it makes no sense that Florida’s financially unsound state retirement program would also expand retirement benefits for many of the more cushy bureaucratic government jobs that can easily be filled by younger, less costly workers, especially for some positions that rarely face any chance of layoffs, pay cuts, or the other potential drawbacks of competitive private sector work.

It would be one thing if government workers were leaving in droves to take more lucrative private sector jobs. But there’s little evidence that is the case. The fact of the matter is that the private sector itself is also experiencing the same workforce shortage across a broad range of industries – and private sector companies already locked in eat-or-be-eaten competition for workers within their own industry cannot also compete against the Florida government for the same talent.

Where are the GOP budget hawks?

Of course every single Democrat on the House Appropriations Committee voted in favor of extending and expanding government benefits paid to our state’s bureaucrats. After all, Democrats never say no to a chance at expanding government.

The real surprise came from the fact that not a single Republican budget hawk exists on the House Appropriations Committee. No GOP committee member expressed the slightest concern about changes that are going to increase the cost of FRS to the state by untold billions of dollars over the coming years if HB 239 passes. The Florida Retirement System (FRS) currently holds a staggering $36 billion in debt, with only 82% of the assets needed to cover long-term benefits. Yet after hearing a parade of law enforcement and first responder union representatives testify in support of expanding their own retirement benefits (no surprise there), not a single member of the Appropriations Committee asked any questions about the bill. The committee members voted 27-0 in favor.

Perhaps now is the time to note that, yes, elected state representatives are also part of the Florida Retirement System. And they can count their years of service in the state legislature toward their overall retirement, which counts in the calculation used to determine the amount of money they get to double-dip in the DROP program, when they eventually qualify. Many lawmakers currently serving will take other elected or appointed government jobs in the coming years, allowing them to qualify for the double-dipping DROP benefits they helped expand.

FRS isn’t getting healthier

Lawmakers voting to feather their own nest is disturbing. But even more disturbing is the fact that the proposed changes will do little to address the shortcomings in the current pension system, which is already woefully underfunded, structurally unsound, and reliant on state contributions and risky investments to stay afloat. Expanding eligibility and increasing retirement payouts, while also increasing interest paid on those double-dipped dollars, is going to cost FRS a whopping amount of money. At the same time, the bill only slightly increases the state’s contribution to FRS itself. That means that over time, the FRS’s unfunded liability – the amount it owes to retirees but can’t actually pay – is only going to grow.

This proposed expansion to the state pension system will cost taxpayers $3.1 billion in the upcoming fiscal year alone. Part of those dollars include a Cost Of Living Allowance (COLA) adjustment that is long overdue for state workers in a rapidly inflating economy. Thankfully, we have the money this year. But will we have it next year? Are lawmakers certain that the state, national and world economies are going to continue to produce budget surpluses that we can lavish on state workers at the expense of the private sector?

In 2011, when then-Governor Rick Scott inherited a state budget that was billions of dollars short thanks to the unforeseen 2008 economic crisis, he and state lawmakers were forced to make tough choices by cutting back on COLA and radically overhauling FRS. While those changes led to a balanced budget, they failed to make the pension system structurally sound. In fact, FRS is even worse off today than it was in 2011.

{kind=link}

Now that we’ve got a budget surplus, a better use of the cash would be to make FRS solvent for the long-haul. Instead, lawmakers are rolling back changes to the system to provide state workers with benefits the private sector cannot afford and does not enjoy. If the economy sputters in the coming years, Florida will be on the hook to pay its retirees because the funds are contractually obligated. That means the cash forked over to retired state employees (and some who are double-dipping), will come from other programs, including education budgets, health care programs, or Florida will have to increase private sector taxation. None of those options are attractive.

As Leonard Gilroy of the Pension Integrity Project at the Reason Foundation points out, “if the system is underfunded, the money has to come from somewhere, and the larger the pension debt grows, the more that pension costs crowd out public services like safety, corrections, and healthcare.”

Florida’s pension system needs a radical overhaul, and it will have to be even more radical if HB 239 is passed. But that requires Republicans with a long term view of the problem and a commitment to do something about it.